The global energy sector is currently navigating its most significant structural shift since the inception of the centralized utility model. As we progress through 2026, the narrative has shifted from “testing” smart grid technologies to “deploying” them at a massive, program-wide scale. According to MarketIntelo, the global smart grid market, valued at approximately USD 35.2 billion in 2024, is projected to expand to nearly USD 102.7 billion by 2033, maintaining a robust Compound Annual Growth Rate (CAGR) of 12.7%. This growth is not merely a reflection of increased demand but a fundamental requirement for a world where intermittent renewables and electric mobility are the new constants.

The Engineering Necessity of Grid Modernization

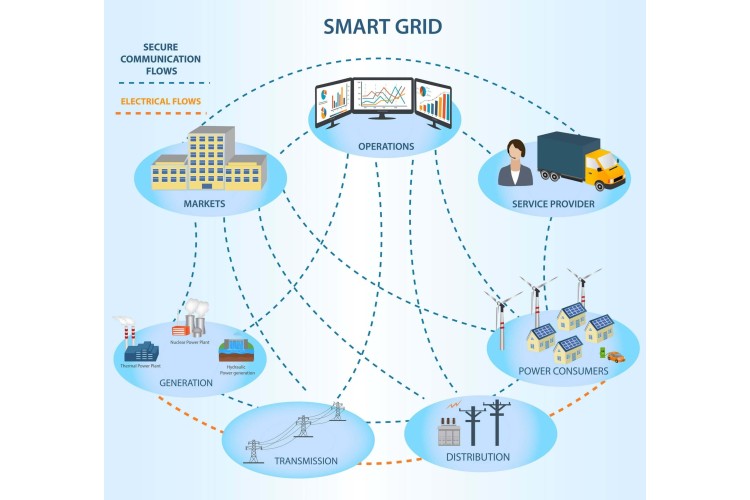

The primary driver behind this market acceleration is the critical need for grid resilience. A significant portion of global power infrastructure is now over 20 years old, designed for a one-way flow of electricity from coal or gas plants to passive consumers. Today’s grid must manage a bidirectional flow, integrating millions of Distributed Energy Resources (DERs) such as residential solar PV and battery energy storage systems (BESS).

From an engineering perspective, this transition relies on Advanced Distribution Management Systems (ADMS). These platforms act as the “brain” of the utility, integrating SCADA, Geographic Information Systems (GIS), and outage management into a single, real-time operational window. By 2026, utilities are increasingly moving toward Cloud-Native Grid Orchestration, allowing for the dynamic balancing of loads that were previously unmanageable.

Digital Twins and Real-Time Telemetry

One of the most transformative trends in the 2026 market is the widespread adoption of Digital Twins for grid infrastructure. By creating a high-fidelity virtual replica of physical assets—from substations to individual transformers—utility operators can run predictive simulations of “high-stress” events.

- Predictive Maintenance: Utilizing IIoT sensors and drone-assisted asset capture, digital twins identify potential line failures before they occur, reducing O&M (Operations & Maintenance) costs by an estimated 15–20%.

- Congestion Management: As EV adoption surges (surpassing 17 million units globally in 2024), digital twins allow operators to simulate the impact of rapid-charging clusters on local transformers, enabling automated load-shedding or demand-response protocols to prevent localized blackouts.

The Role of 5G and Edge Intelligence

Communication remains the backbone of the smart grid. In 2026, the focus has shifted toward 5G Standalone (SA) Networks to support Ultra-Reliable Low-Latency Communications (URLLC). Traditional communication protocols often suffered from latency that made real-time grid “self-healing” difficult.

5G enables Edge Intelligence, where decision-making happens at the substation or even the smart-meter level, rather than waiting for a round-trip to a centralized data center. This sub-millisecond response time is essential for Frequency Regulation, especially in grids with high solar and wind penetration, where power supply can fluctuate within seconds due to cloud cover or wind gusts.

Regional Market Dynamics: The India Perspective

In the Indo-Pacific region, and specifically within India, the smart grid market is witnessing an unprecedented push driven by policy and necessity. The Revamped Distribution Sector Scheme (RDSS) has set the stage for a nationwide rollout of smart meters, targeting the replacement of 250 million conventional meters.

For Indian utilities, the goal is twofold: reducing AT&C (Aggregate Technical and Commercial) losses and improving the financial viability of Discoms. Market data indicates that India is becoming a global hub for smart grid hardware manufacturing, with significant investments in Advanced Metering Infrastructure (AMI) and localized software solutions for grid cybersecurity.

Strategic Challenges: Cybersecurity and Interoperability

As the grid becomes more digitized, it also becomes more vulnerable. In 2026, Cyber-Physical Security has moved from a “check-box” exercise to a core market segment. The integration of legacy IT (Information Technology) with modern OT (Operational Technology) creates “air-gap” vulnerabilities that sophisticated threat actors exploit.

The industry is responding with Zero-Trust Architecture and Blockchain-based energy transactions. By utilizing a decentralized ledger, utilities can secure the data exchange between millions of connected devices, ensuring that every kilowatt-hour of energy traded—whether from a home battery or a utility-scale wind farm—is verified and tamper-proof.

The global smart grid market is characterized by a sophisticated structural framework that allows for a comprehensive analysis of its growth and impact. To provide a clear overview for the article, the market can be broken down into the following strategic segments:

- Market Components: The ecosystem is fundamentally comprised of Hardware (sensors, smart meters), Software (data analytics, management platforms), and Services (consulting, maintenance, and integration).

- Technological Architecture: Core innovations driving the market include Advanced Metering Infrastructure (AMI), Distribution Automation, Transmission Upgrades, and Substation Automation, alongside various emerging grid-edge technologies.

- Application Sectors: Solutions are tailored for diverse environments, specifically categorized into Residential, Commercial, and Industrial applications to meet varying energy density needs.

- Deployment Models: Organizations choose between On-Premises infrastructure for localized control or Cloud-based solutions for enhanced scalability and remote data management.

- Primary End-Users: The market caters to a wide-ranging consumer base, including large-scale Utilities, as well as the Industrial, Commercial, and Residential sectors seeking improved energy efficiency.

- Geographic Scope: Market activity is monitored across all major global regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Investment and Policy Support

The financial landscape for smart grids is currently bolstered by landmark policies such as the European Green Deal and the U.S. Grid Resilience and Innovation Partnerships (GRIP) program, which recently injected USD 10.5 billion into modernization efforts. Globally, annual investment in electricity grids needs to rise from the current USD 300 billion to over USD 600 billion by 2030 to stay aligned with Net-Zero pathways.

Conclusion: Toward an Autonomous Grid

The smart grid of 2026 is no longer just a collection of “smart meters.” It is an evolving, autonomous ecosystem that senses, reacts, and heals in real-time. As utilities move away from static infrastructure, the synergy between hardware (sensors and smart transformers) and software (AI and 5G) will determine the reliability of our energy future.

For stakeholders, the message is clear: The “Smart Grid” is the essential infrastructure of the Fourth Industrial Revolution. Those who invest early in interoperable, data-driven systems will be the leaders of the new energy economy, while those who cling to legacy models risk becoming obsolete in an increasingly electrified world.