The global maritime industry is standing at a historic crossroads, transitioning away from heavy fuel oils toward a zero-emission future. Central to this transition is the green hydrogen bunkering infrastructure market, which is emerging as the backbone of sustainable shipping logistics. As the International Maritime Organization (IMO) tightens its greenhouse gas (GHG) emission targets for 2030 and 2050, the demand for scalable hydrogen refueling systems has shifted from experimental concepts to a critical infrastructure asset class. By 2033, this market is projected to play a decisive role in decarbonizing the 3% of global CO2 emissions currently attributed to maritime trade.

The Economic Trajectory: 2026–2033

The financial landscape for the green hydrogen bunkering infrastructure market is fueled by an aggressive compound annual growth rate (CAGR), with recent research suggesting the broader green hydrogen sector will reach a valuation of USD 8.1 billion by 2034. For bunkering specifically, growth is being concentrated in major maritime hubs—such as the Port of Rotterdam and Singapore—where port authorities are investing heavily in Proton Exchange Membrane (PEM) electrolyzers to produce hydrogen on-site.

According to Market Intelo, the global green hydrogen bunkering infrastructure market was valued at $1.2 billion in 2025 and is projected to reach $8.1 billion by 2034, expanding at a robust compound annual growth rate (CAGR) of 24.0% over the forecast period 2026-2034.

This regional growth is particularly evident in the Asia-Pacific region, which is expected to dominate nearly 41% of the market share by 2026. India, in particular, is positioning itself as a global hydrogen hub, leveraging its falling solar PV costs to power the electrolysis needed for high-capacity bunkering stations.

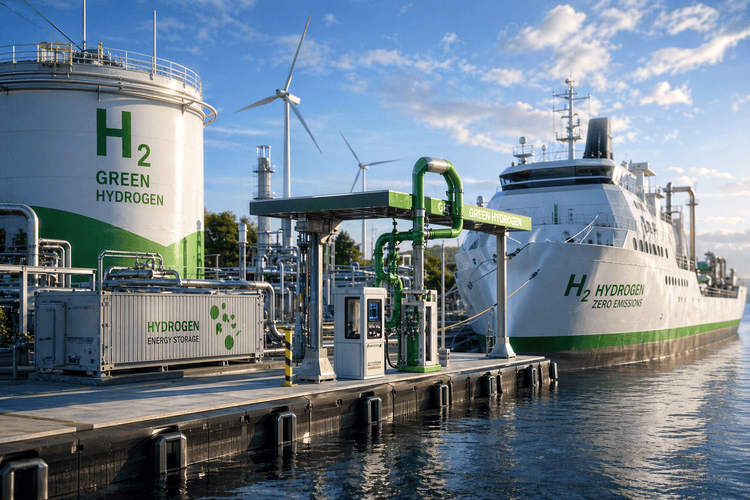

Technical Architecture: Engineering the Fuel of the Future

Successfully efficiently managing teams and projects in the construction of these facilities requires a deep understanding of the mechanical logic behind hydrogen storage. Unlike traditional fuels, green hydrogen requires specialized infrastructure to handle its unique physical properties:

- Cryogenic Storage & Handling: Managing liquid hydrogen at temperatures of -253°C requires vacuum-insulated piping and advanced thermal management systems.

- PEM Electrolyzer Integration: These systems offer the high response times necessary to work with intermittent renewable sources like solar and wind, ensuring a 100% green supply chain.

- Safety and Monitoring: Modern bunkering stations are increasingly integrated with AI-driven digital twins to monitor pressure and temperature in real-time, preventing failures before they occur.

Strategic Market Segmentation

The green hydrogen bunkering infrastructure market is currently segmented by several key technical factors:

- Technology Type: Dominance of PEM and Alkaline electrolyzers for on-site production.

- End-User Applications: Primarily focused on container ships, bulk carriers, and tankers that require high-density energy for long-haul routes.

- Distribution Channels: A mix of on-site production at ports and centralized production hubs that transport hydrogen via specialized carriers.

Conclusion: A Decade of Transformation

The coming decade will define the winners in the maritime energy transition. For port operators and technical professionals, the green hydrogen bunkering infrastructure market represents more than just a refueling solution; it is a strategic investment in the future of global trade. By prioritizing the development of robust infrastructure today, the industry can ensure that the zero-emission vessels of 2030 have the reliable, clean energy they need to power the world’s economy.

Regional Market Intelligence and Research Support

This comprehensive green hydrogen bunkering infrastructure market study by MarketIntelo provides in-depth insights into market size, deployment models, component segmentation, application trends, regional performance, and competitive positioning through 2033.