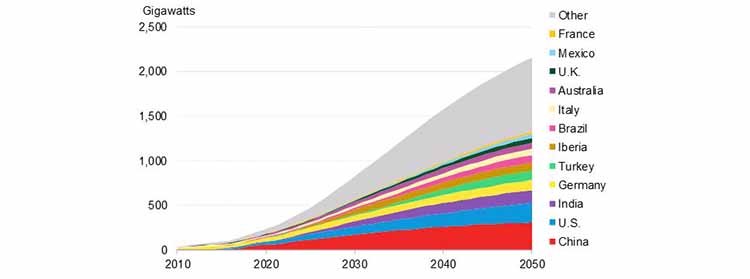

MISSISSAUGA – Customer-sited solar is a major untapped opportunity, which could see 167 million households and 23 million businesses worldwide hosting their own clean power generation by 2050, according to a joint report by research firm BloombergNEF (BNEF) and Schneider Electric. These deployments will unlock major decarbonization benefits, but policy and tariff design will be critical to enable them.

The report ‘Realizing the Potential of Customer-Sited Solar’ finds that rapidly falling costs of solar technology have already made it economical for homes and businesses to generate their own power in some markets. In Australia, for example, the payback period for households investing in solar has been favorable, at less than 10 years, since 2013. As a result, adoption has already taken off, with more than 2.5 gigawatts of residential solar added in 2020 alone.

These solar installations can generate economic returns for the hosting homes and businesses, as well as wider benefits in terms of carbon emissions reductions, peak load reductions, and employment opportunities.

“Customer-sited solar is a huge opportunity that’s often completely overlooked. Thanks to falling costs and policy measures, it’s already being rapidly deployed in some markets. Its massive scale up is very likely,” said Vincent Petit, Head of the Schneider Electric TM Sustainability Research Institute, and SVP of Global Strategy Prospective & External Affairs at Schneider Electric. “This is vital for decarbonizing the power sector and offers huge additional consumer benefits. It’s time to embrace this transformation.”

Kick-starting the market

Experience shows that solar adoption mainly occurs when there is an economic case for the households and businesses investing in the technology, usually in the form of high internal rates of return (IRR) or short payback periods. In regions where the economics have not yet reached such tipping points, policy makers are introducing targeted incentives to create favorable market conditions and bring forward deployment.

One such example is France, where existing incentives mean that residential solar can earn internal rates of return of around 18.5% (a five-year payback), and commercial installations achieve 10.4% IRR (or a nine-year payback). This has stimulated gradual growth in the market, to about 500 megawatts of installations in 2020.

A key consideration at the early stage of market development is to avoid an unsustainable boom. Policy designs should account for the fact that solar costs will continue to fall over time, and moderate support to reflect these changing dynamics.

Solar for new-build homes and businesses

The economic case for adding solar during construction of new buildings is particularly strong. This is because so-called ‘soft costs’, such as marketing and sales costs, as well as labor and construction costs, can be reduced, while the benefits remain the same. In California, the economic case for adding residential solar on existing homes is already good at 20% IRR, but the new report estimates that this figure is twice as high, at 40% IRR, when solar is added at the point of construction. In France, the IRR for residential solar could be boosted to 28% when added during new construction.

Introducing energy storage and flexibility

As solar markets develop and mature, policy makers and regulators must gradually shift their emphasis toward unlocking flexibility and encouraging the adoption of energy storage. This is because high levels of solar adoption can lead to excess energy production during the day, while also possibly destabilizing the power grid. At this stage, the addition of energy storage becomes valuable, as it allows the renewable electricity to be stored for use during evening hours.

“The evolution of customer-sited solar is to add some form of flexibility, which has the ability to unlock a much higher penetration of solar,” said Yayoi Sekine, BNEF’s Head of Decentralized Energy. “The most obvious form of flexibility is batteries, but energy storage will come in many forms, including shifting demand and using electric vehicles.”

Tools to encourage energy storage include adjusted export rates (the payments offered to solar owners when they export energy to the grid), time-of-use retail electricity rates (which reflect the lower generation costs of solar during the daytime), enabling payments for storage to provide grid services (sometimes called aggregation payments), and implementation of demand charges (primarily for business customers). These levers are generally meant to make rates more reflective of generation and grid costs but are also likely to encourage energy storage.

In California, for example, reducing export rates to 35% of retail tariffs, while it would damage the economics of solar overall, would shift the emphasis over to solar systems paired with storage, which would still generate a 13% IRR. For commercial and industrial installations, adding so-called aggregation payments for batteries would boost IRRs to 22.8%, making solar-plus-storage a more attractive option than solar alone.